MSMEs vs Global Giants, How AI Lets You Compete Head On

February 20, 2026

1.Introduction – Indian Steel Industry: Current Scenario and Future Outlook

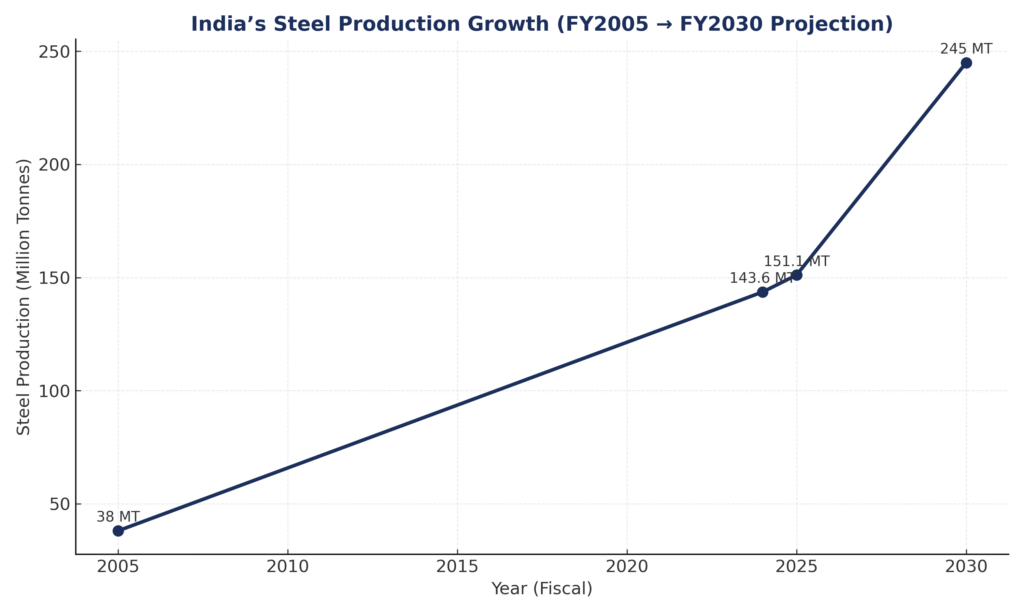

India is fast emerging as a powerhouse in global steel production, and the latest figures reinforce this trend. In FY 2024 (April 2023 – March 2024), India produced 143.6 million tonnes (MT) of finished steel. Building on that momentum, in FY 2025, steel output rose further to approximately 145.3 MT (finished steel) and 151.1 MT (crude steel)steel.gov.inReuters+1.

To truly appreciate the scale of this growth, consider this: in FY 2005 (April 2004 – March 2005), India’s steel production was just 38 MT. In two decades, the output has nearly quadrupled—a stunning industrial leap Wikipedia.

Fueled by massive infrastructure expansion, from highways and ports to rail projects and urban developments, steel is the backbone of India’s economic transformation. Projections indicate that by 2030, steel production could reach 240–250 MT, further cementing India’s global steel leadership.

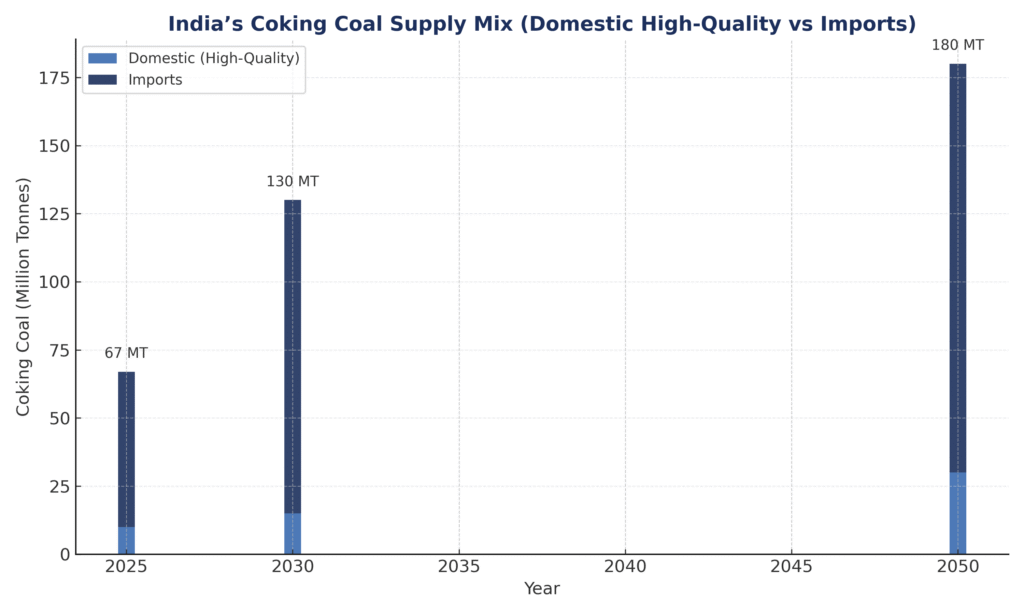

Despite having abundant iron ore reserves, India remains heavily dependent on imports of high-quality coking coal, essential for the blast furnace–basic oxygen furnace (BF-BOF) steelmaking process. Typically, crafting one tonne of steel requires about 0.8–0.9 tonnes of coking coal—making coal access a key lever to maintain growth in steel output.

With most major Indian steelmakers still using the BF-BOF process, demand for imported coking coal stays closely tied to steel expansion plans. Among global suppliers, the United States is now emerging as a strategic partner, offering both opportunities and challenges for India’s steel industry.

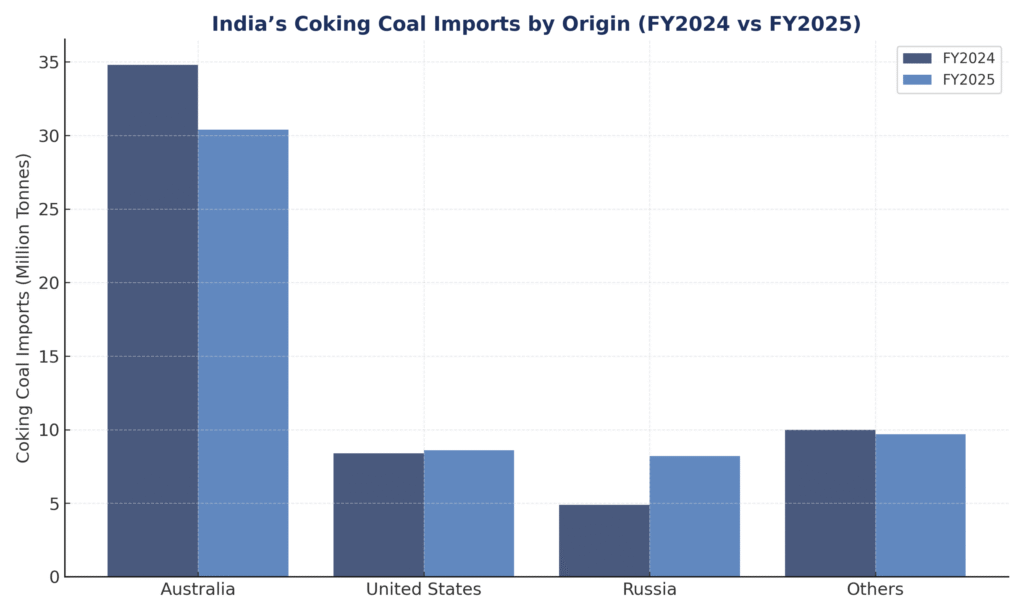

In summary, while Australia remains dominant, the United States is carving out a larger role, and Russia is emerging as a third strong pillar of India’s coal supply base. This shifting mix underscores the importance of diversifying away from a single supplier and building long-term resilience.

2. India’s Current Coking Coal Imports – A Country-wise Breakdown1.

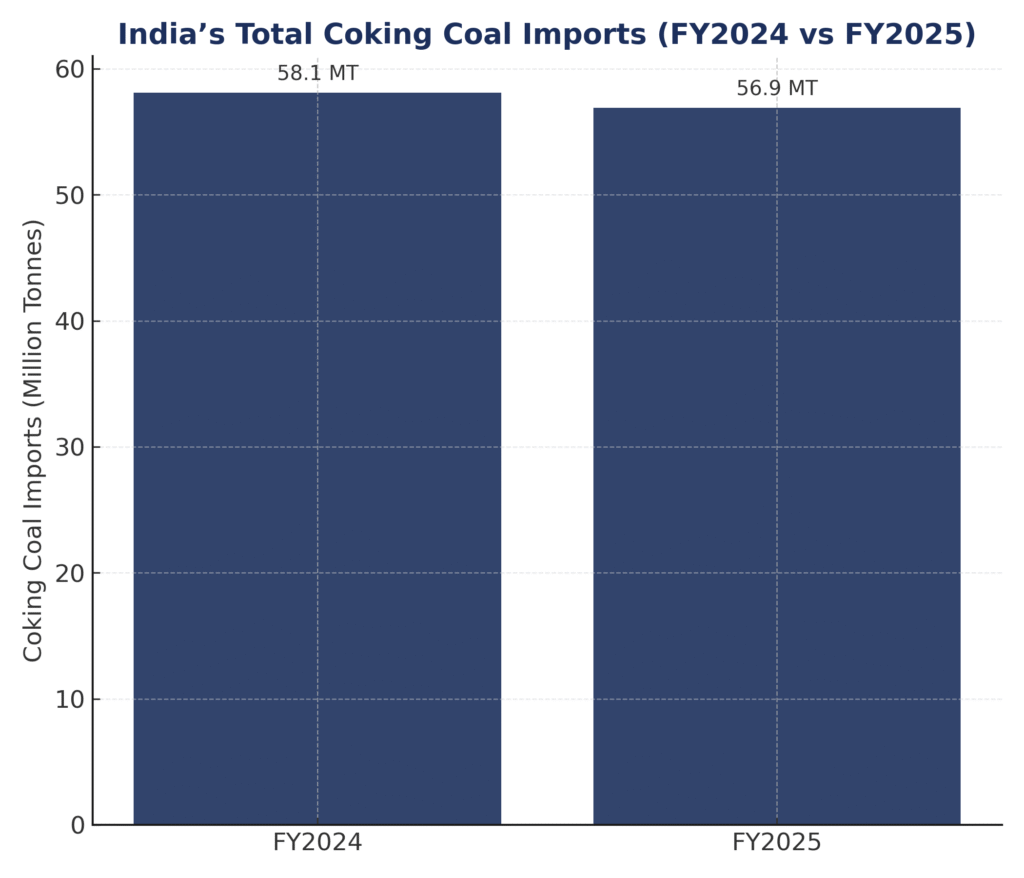

India’s dependence on imported coking coal remains one of the defining features of its steel industry. Despite efforts to boost domestic mining, the country still sources the bulk of its metallurgical coal requirements from overseas markets. In FY 2024 (April 2023 – March 2024), India imported around 58.1 million tonnes (MT) of coking coal, a slight increase from previous years. The supply base, however, remains concentrated among a handful of exporters. Australia continues to dominate, accounting for nearly 60% of India’s coking coal imports. Its premium hard coking coal remains the preferred choice for Indian blast furnaces. Yet, overreliance on Australia has exposed Indian steelmakers to risks, as extreme weather events in Queensland repeatedly disrupted supply chains and caused price volatility. The United States has emerged as the second-largest supplier, exporting about 8.4 MT in FY 2024, or nearly 14% of India’s total imports. This marks a growing share compared to earlier years, highlighting how U.S. coal is becoming a serious alternative for Indian mills seeking both quality and diversification. Other notable suppliers include Russia, Canada, Mozambique, and Indonesia, together contributing close to 15 MT. Russia’s share has risen in recent years as Indian buyers look for additional flexibility amid global trade realignments. To illustrate:-

- Australia: ~34.8 MT (≈60% of imports)

- United States: ~8.4 MT (≈14% of imports)

- Others (Russia, Canada, Mozambique, Indonesia, New Zealand, etc.): ~14.9 MT (≈26% of imports)

From a port perspective, Paradip remains India’s largest coking coal gateway, followed by Vizag, Dhamra, and Haldia. On the company side, SAIL and JSW Steel continue to be leading buyers, with JSW even surpassing others in individual months.

{kind=link}

{kind=link}

{kind=link}