Pax Silica Explained: How India’s New Alliance Changes the AI Game

March 2, 2026

Stay Profitable in Chaos: MSME Survival Plan for the Gulf Crisis

This guide gives MSMEs a survival plan for the 2026 Gulf crisis, turning oil shocks, shipping delays and cash‑flow stress into a clear, data‑driven action plan you can execute this week.

Oil has jumped sharply in just a few days, and MSMEs are directly in the line of fire.

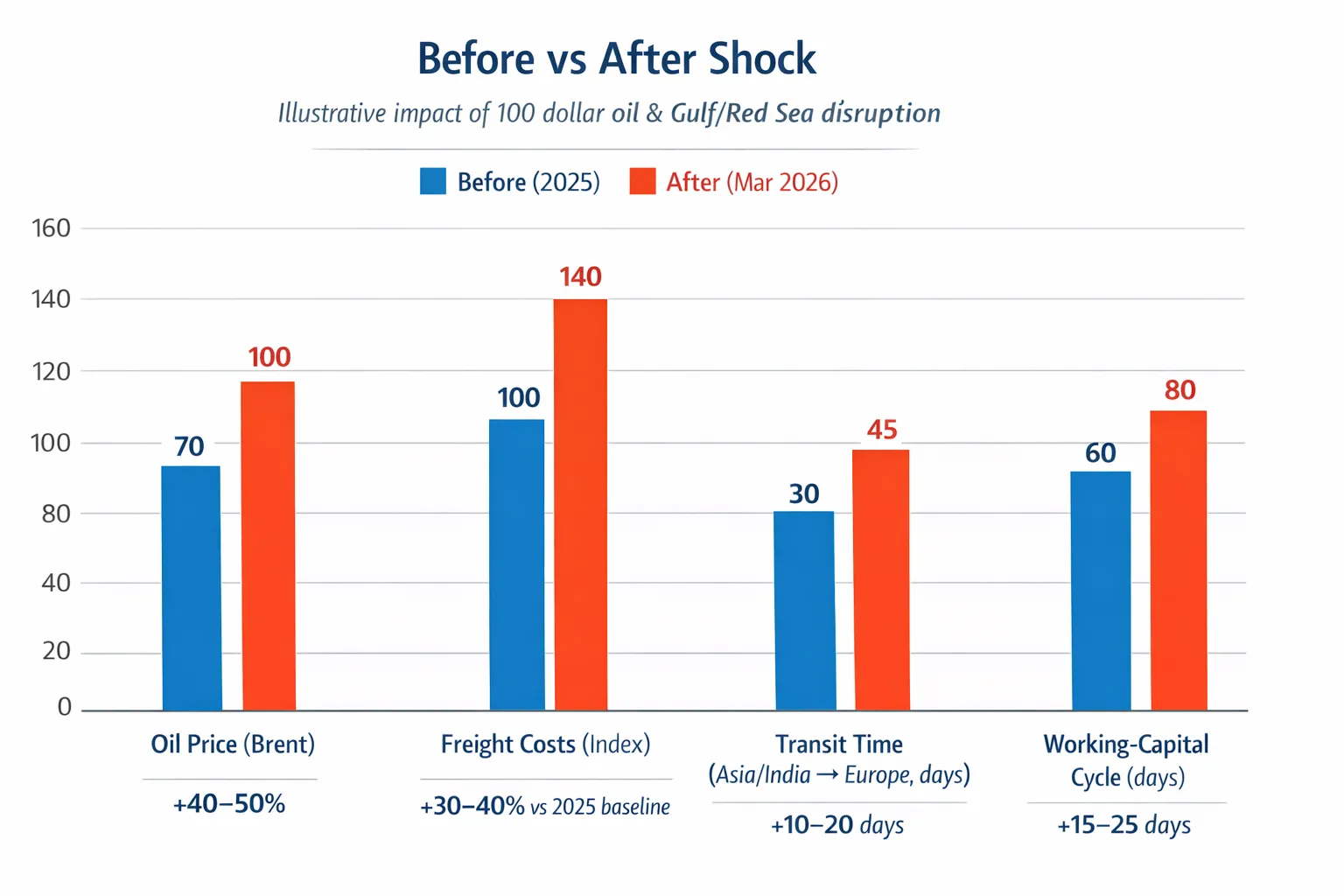

Between 26–27 February and early March, Brent crude has risen roughly 10–15%, moving from the low‑70s USD per barrel (around 70–72) to around 80–82 USD per barrel, and has since surged above 100 USD as markets fully price in the Hormuz shutdown risk. At the same time, European gas and LNG benchmarks have spiked; front‑month Dutch TTF gas prices have jumped more than 25% in a single day and are now trading several tens of percent above late February levels, with scenario analysis showing they could temporarily rise to around 90 EUR/MWh if Gulf LNG disruptions extend.

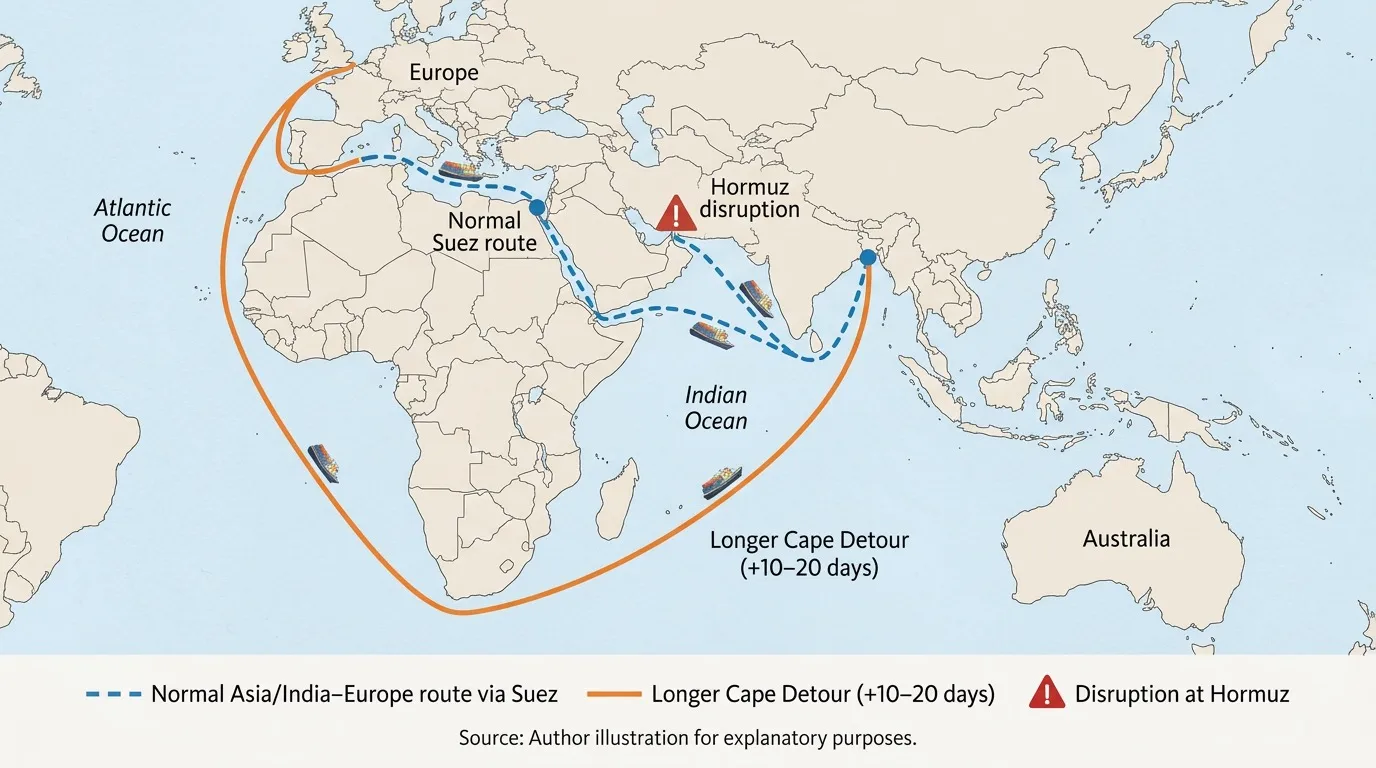

Major shipping lines have reduced or suspended calls at Gulf ports and are rerouting vessels around the Cape of Good Hope, effectively halting transits through the Strait of Hormuz and adding 10–20 days on some Asia–Europe routes. War risk insurance premia for tankers and container vessels in the region have also jumped sharply, with some quotes up roughly ten‑fold versus pre‑crisis levels and war‑risk or hull‑war rates rising on the order of 25–50% or more, as underwriters cancel or reprice coverage.

If you are an MSME, exporter, importer, or trader, this is not abstract macroeconomics. This is your input cost, your freight bill, and your cash flow cycle.

I have formulated this survival plan for you as if I were a part of your company. No sermons, only actionable plans, deciding which levers to pull this week.

The Shock in Numbers: What Changed in Days

Let’s get the core metrics on the table first.

- Around 26–27 February, Brent crude was trading in the low‑70s USD per barrel (≈70–72), a price level that reflected “normal” geopolitical risk, not panic.

- Following escalation involving Iran, attacks and threats around key energy routes, and direct threats to shipping around the Strait of Hormuz, Brent quickly moved above 80 USD per barrel in early March and has since broken above 100 USD as disruption fears intensified.

- That’s a double‑digit percentage move in a handful of trading sessions is what traders call “risk premium being repriced” as markets embed the probability of supply disruption.

On the gas and LNG side:

The Middle East supplies a large share of global LNG, with Qatar alone accounting for roughly 20%+ of global LNG exports in recent years, so disruption there feeds directly into benchmark prices.

Scenario and market analyses now show that a prolonged Strait of Hormuz disruption could push Europe’s TTF gas benchmark towards or above 90 EUR/MWh, roughly tripling from around the low‑30s EUR/MWh base case, while spot prices have already jumped more than 25% in a single session as the crisis escalated.

On shipping and logistics:

- Several global container and tanker operators have scaled back or suspended calls at key Gulf ports due to security concerns and insurance costs, with leading container lines halting transits through the Strait of Hormuz.

- Vessels are being rerouted via the Cape of Good Hope instead of Gulf/Suez–linked routes, extending Asia–Europe transit times by roughly 10–20 days and increasing fuel and charter costs.

- War‑risk premiums and freight rates on routes exposed to the Gulf have surged as insurers and shipowners reprice risk; seven‑day war‑risk cover quotes for some vessels have risen around ten‑fold and can reach around 1–10% of hull value in high‑risk profiles.

In one line for MSMEs: your energy is more expensive, your logistics are slower and riskier, and your cash will sit at sea longer.

Why the Strait of Hormuz Shock Is Different

This is not just “another” Middle East headline. The Strait of Hormuz is one of the most critical chokepoints in global energy and trade.

- In recent years, estimates suggest around a quarter of global seaborne crude oil trade,about 20 million barrels per day moves through the Strait of Hormuz, equivalent to roughly 25% of global seaborne oil flows.

- A significant share of global LNG exports, including a major portion from Qatar, also transit this narrow waterway, and over 80% of the crude oil and LNG passing through is destined for Asian markets.

When flows through Hormuz are threatened, three layers of shock hit simultaneously:

- Oil and refined products: Reduced or threatened throughput leads to higher prices, adding an immediate cost layer to diesel, bunker fuel, and many petrochemical derivatives.

- Gas and LNG: LNG cargoes are delayed, rerouted, or repriced, causing gas benchmarks to spike, especially in gas‑import‑dependent regions like Europe and parts of Asia.

- Container trade and general cargo: Gulf ports serve as trans‑shipment and distribution hubs linking Asia, the Middle East, and Europe. Disruption there forces rerouting and delays across multiple trade lanes, not just energy.

For an MSME, this is not an academic supply chain puzzle. It translates into:

- Higher input prices for energy‑intensive materials (chemicals, plastics, metals, fertilizers).

- Longer transit times, which stretch working capital cycles.

- Higher freight and insurance costs on affected lanes.

The right question is not “is this good or bad news,” but:

- Where is my direct exposure? (Products, inputs, lanes that clearly touch the Gulf or energy derivatives.)

- Where is my hidden exposure? (Suppliers or customers who rely on these routes or fuels even if you do not see it directly.)

- What can I still control? (Pricing, contracts, suppliers, routing, cash, collaboration.)

Lessons from the Black Sea: The Adjustment Always Hurts Smaller Players More

We have seen a similar pattern in another region: the Black Sea after Russia’s invasion of Ukraine.

- Following the invasion, grain and other commodity exports from Black Sea ports dropped sharply, with hundreds of merchant vessels stranded or delayed.

- Freight rates and maritime insurance costs increased, reflecting heightened risk and logistical constraints.

- Importing countries and large buyers eventually diversified to alternative origins (e.g., Brazilian and U.S. grain) and alternative routes (rail, river corridors through Eastern Europe), but this took months and added cost.

The pattern:

- The global system eventually adjusts, but

- Small and mid‑size firms with thinner capital buffers, weaker bargaining power, and less access to information, pay the highest price during the adjustment phase.

The Hormuz scenario is more systemic:

- It impacts oil, gas, petrochemicals, and key Asia–Europe trade routes all at once, unlike the more commodity‑specific Black Sea grain disruption.

For MSMEs, the takeaway is clear: you cannot wait for the system to “normalize.” You must actively re‑shape your own risk profile now.

The 5‑Pillar Survival Plan for MSMEs

How Hormuz disruption forces Asia–Europe cargo to detour via the Cape, adding 10–20 days and extra fuel and freight costs

What follows is a five‑pillar checklist you can apply directly inside your business. You will not fix everything in one week and that’s fine. If you move decisively on even two pillars in the next 7–10 days, you materially improve your odds of surviving this shock and the next one.

The pillars are:

- Map Your Risk

- Fix Your Contracts and Force Majeure

- Protect Your Cash and Margins

- Do Not Fight Alone—Cooperate

- Use Data Like a Trader

Pillar 1 – Map Your Risk (Not Diversify Blindly)

Don’t wait for normalcy, sit with your team, map your exposure, and decide what changes this week.

Most advice jumps straight to “diversify.” But for MSMEs, Pillar One is measurement, not diversification. You cannot diversify intelligently until you know exactly where the risk sits.

Set aside an evening with your team, a spreadsheet, or even pen and paper, and capture the following:

a) Revenue concentration

- List your top five products, and for each, calculate what percentage of total revenue it contributes.

- If any single product or segment contributes more than 30–35% of total revenue, flag it red as a concentration risk.

b) Input and sourcing risk

For each key product:

- List the critical raw materials or inputs.

- For each input, note the supplier, country/region of origin, and whether the supply chain crosses the Middle East or depends on Gulf logistics.

- If any critical input comes from a single supplier or a single geography, flag it red. Single points of failure are dangerous in times of disruption.

c) Logistics and route risk

- Identify which of your import or export shipments rely on:

- Gulf ports as trans‑shipment or destination hubs.

- Routes that transit near or through the Strait of Hormuz or adjacent high‑risk zones.

- Note the usual transit time for each of these lanes.

- If more than ~40–50% of your shipping volume is dependent on Gulf‑linked or Hormuz‑sensitive routes, flag that portfolio red.

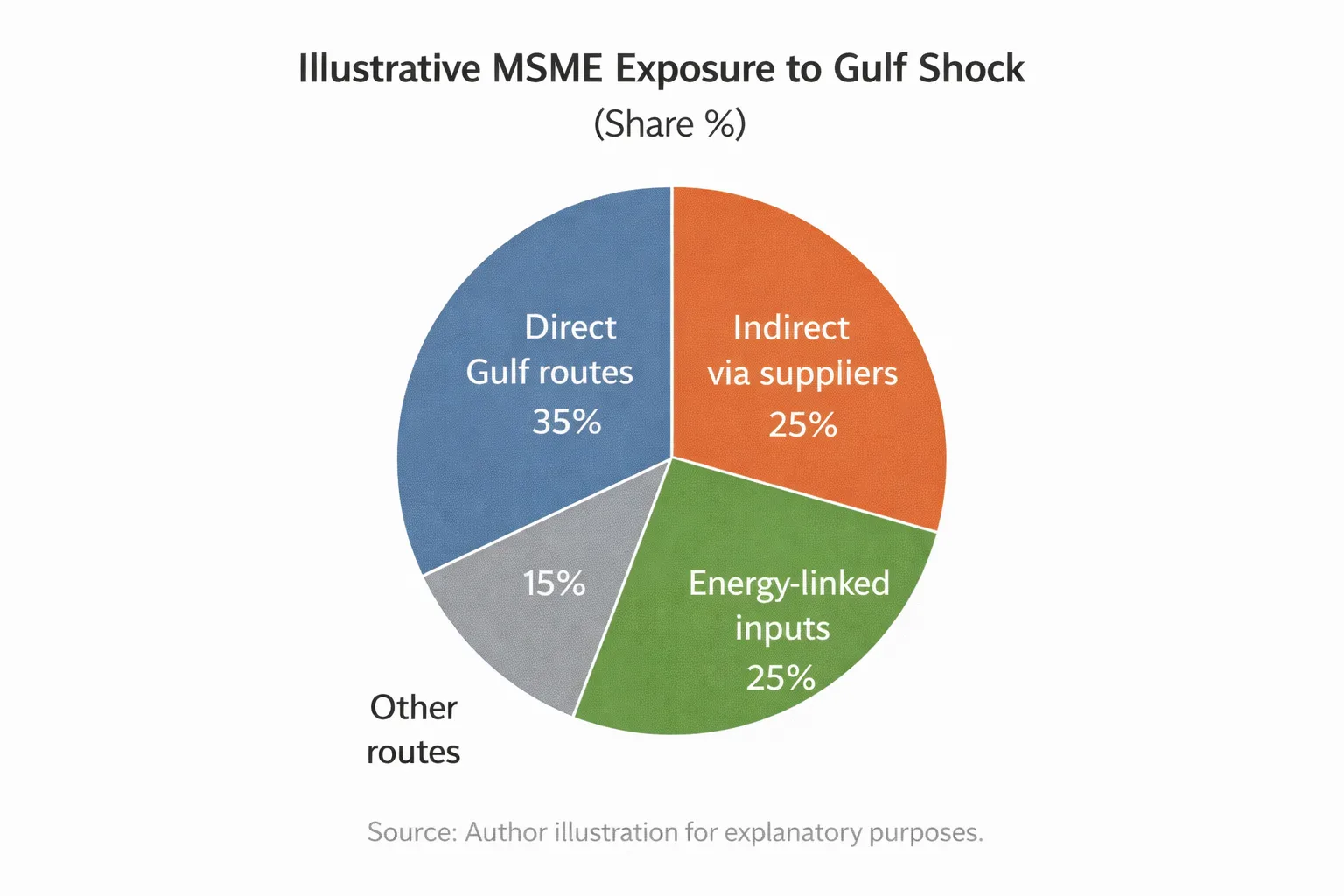

Once you’ve done this, you have a basic risk heat map.

Illustrative breakdown of how a typical MSME’s exposure to the Gulf shock can be split across routes and inputs (for planning, not forecasting).

Turning the map into action:

- For heavily exposed products, identify one or two adjacent products (similar customer base, similar capabilities) that rely on less energy‑sensitive inputs or routes not tied to the Gulf. Start scoping them now, not next quarter.

- For each red‑flag input, identify at least one alternate supplier in a different geography (e.g., Southeast Asia, Africa, Latin America, or domestic).

- Even if their quote is 3–5% higher, treat that incremental cost as an insurance premium, not as “wasted margin.”

- Ask your freight forwarder or logistics partner for alternative routings on your highest‑value lanes and record the extra days and extra cost.

This is 2–3 evenings of work that can change your risk profile for years.

Pillar 2 – Fix Your Contracts and Force Majeure

Pillar Two is less glamorous but absolutely critical: your contracts.

Many MSMEs neglect contract language until they are already in trouble. In a shock like this, you must assume that some contracts will become impossible or uneconomic to perform. Your first line of defense is the text you have already signed.

Review your key sales and purchase contracts and check three things immediately:

1. Scope of the force majeure clause

Confirm that force majeure explicitly covers:

- War and armed hostilities in relevant regions.

- Blockade, closure, or material disruption of key maritime routes (e.g., Strait of Hormuz, Suez‑linked corridors).

- Government‑imposed export or import bans, sanctions, or embargoes that affect your ability to ship or receive goods.

If these are not explicitly listed, your ability to invoke force majeure may be contested.

2. Notice and procedure :

Check whether the clause clearly answers:

- How you must notify the counterparty (e.g., written notice, email, registered letter).

- Within how many days of the event you must send that notice.

- What happens during the period of force majeure:

- Are obligations suspended?

- For how long?

- What happens if the event continues beyond a defined number of days (e.g., right to terminate or renegotiate)?

3. Evidence and internal process

Internally, you need:

- A standard email template or letter for force majeure notices.

- A digital evidence folder (e.g., shared drive, DMS) where you store:

- Carrier or shipping line suspension notices.

- Port closure or restriction advisories.

- Government circulars, sanctions notices, or trade advisories.

- Insurance communication relating to war‑risk surcharges or restrictions.

Example: if your carrier emails, “Shipments via [Gulf port] are suspended due to hostilities,” that email is saved in the evidence folder and attached to your force majeure notice to customers or suppliers.

This is exactly how larger companies protect themselves from penalties and litigation. MSMEs cannot afford to treat this as optional.

Pillar 3 – Protect Your Cash and Margins

When energy and freight spike, three things happen to your P&L and balance sheet:

- Input costs rise (energy‑linked raw materials, packaging, transport).

- Shipping and logistics costs rise (freight, insurance, surcharges).

- Cash is tied up for longer because goods spend more time in transit.

Here is how to respond at MSME scale.

➡️ Price and contract structure

Wherever you have even moderate bargaining power:

- Shift from fixed prices to prices with adjustment bands. For example:

- “If Brent crude moves more than X USD per barrel from today’s level, we will review and adjust the price based on an agreed formula.”

- Alternatively, index part of your price to a transparent benchmark (e.g., a polymer index, bunker fuel index, or regional freight index), with a clear formula and reference source.

- This approach is standard in commodity contracts and allows you to share volatility with buyers or suppliers instead of absorbing it all.

In periods of high volatility:

- Avoid 12‑month fixed‑price contracts unless: You have matching hedges (e.g., commodities futures) or

- Strong contractual pass‑through mechanisms with your own suppliers.

- Prefer 3–6‑month contracts with explicit review or reopeners triggered by defined volatility thresholds.

➡️ Working capital and transit time

If a lane that usually takes 25 days is now taking 40 days via a reroute, that is 15 extra days of:

- Inventory in transit.

- Receivables collection delay (if you invoice on delivery).

Practical steps:

- Calculate your current average receivable days and average inventory days (simple averages are fine).

- Add 15–30 days to this, depending on your exposure to rerouted lanes.

- Ask, honestly: “Can we survive an extra 15–30 days of cash cycle if these conditions persist for 3–6 months?”

If the answer is no:

- Proactively speak to your bank, NBFC, or fintech lender about:

- Invoice discounting on confirmed receivables.

- Export factoring tied to confirmed overseas orders.

- Short‑tenor working capital lines specifically structured around longer transit times.

The goal is straightforward: do not run out of oxygen (cash) because ships are taking a longer, safer route.

Pillar 4 – Don’t Fight Alone: Build Collective Power

Alone, you are a small shipper. Together, a cluster of MSMEs can behave more like a mid‑size client to logistics providers, banks, and even policymakers.

Three concrete moves:

- Form or join a logistics/transport group in your cluster

- Within your industrial area or trade association, create a logistics working group.

- Pool your freight volumes to negotiate:

- Better freight rates on key lanes.

- More reliable access to space on alternative routes (e.g., non‑Gulf trans‑shipment hubs, Cape routes).

- Share real‑time information

- Use a simple WhatsApp/Signal group, email list, or weekly call to share:

- Delays by route and port.

- New surcharges imposed by shipping lines or forwarders.

- Local port, customs, or regulatory issues that others might face next.

- Information that sits in one MSME’s inbox is a lost asset. Shared, it becomes a collective risk radar.

- Build a data pack for advocacy and negotiation

Track and document:- Actual delay days per lane (before vs after crisis).

- Extra freight and insurance costs per shipment.

- Number and value of orders cancelled, delayed, or renegotiated due to the crisis.

Use this

- In conversations with banks and financiers to justify temporary relaxation of covenants or additional working capital.

- In discussions with insurers about coverage and premium adjustments.

- Through industry bodies when engaging with policymakers on relief measures, credit guarantees, or export support.

Large companies already do this via formal industry chambers and lobby groups. MSMEs need to start treating information and pooled volume as shared strategic assets, not as proprietary secrets.

Pillar 5 – Use Data Like a Trader (Not Like an Influencer)

The fifth pillar is about digital tools and AI, but used with a trader’s mindset, not for vanity metrics.

➡️ Sourcing and market discovery

- Use B2B platforms, trade databases, and AI‑powered sourcing tools to scan for alternative suppliers and buyers in regions less exposed to Gulf disruptions.

- Filter potential partners by: Country risk and logistics exposure. Tariffs and trade agreements relevant to your country. Lead times, minimum order quantities, and reliability indicators (on‑time performance, dispute history where available).

➡️ Scenario planning

Build simple “what if” models for your top 5 products:

- Scenario A – Oil at 80 vs 100 USD/barrel:

- Estimate how fuel surcharges, input costs, and freight might change.

- Calculate the resulting margin per product and at portfolio level.

- Scenario B – Transit time +20 days:

- Estimate the additional working capital needed.

- Identify which customers or contracts become uneconomic under these conditions.

This can be done with basic spreadsheets; AI can assist in building or checking these models.

➡️ Documentation and retrieval

- Store contracts, purchase orders, shipment documents, and key correspondence in a searchable, backed‑up system (cloud DMS, well‑structured shared drive).

- Tag documents by:

- Counterparty, product, route, and date.

- Whether they contain force majeure, price adjustment, or termination clauses.

When disruption hits, you should be able to retrieve the relevant contract and evidence in minutes, not days. That speed can be the difference between absorbing a loss and successfully enforcing a contractual protection.

This is not about being “tech‑savvy.” It is about making decisions with better, faster information than your competitors.

Mindset Shift: You Can’t Control Crises, Only Your Response

You cannot control:

- Wars or geopolitical escalations.

- Whether the Strait of Hormuz is open, partially blocked, or effectively closed.

- The exact path of oil, gas, freight, or insurance prices over the next few weeks.

But you can control:

- How concentrated your risk is across products, customers, inputs, and routes.

- How your contracts read, especially around force majeure and price adjustments.

- How your cash cycle is structured, and whether you have backup lines of liquidity.

- Who you cooperate with or whether you choose to fight alone.

- How quickly you see and react to information, compared with your peers.

Your Middle East Shock Checklist for MSMEs

To make this operational, you can turn the five pillars into a simple internal checklist:

- Risk Mapping: Top 5 products, revenue share, red‑flag concentrations, input and route risks identified and documented.

- Contracts & Force Majeure: Key contracts reviewed, gaps noted, templates and evidence folder set up.

- Cash & Margin Protection: Price bands/indexation discussed, contract terms shortened, cash‑cycle impact quantified, financing options lined up.

- Cooperation: Logistics group formed or joined, information‑sharing channels active, data pack under construction.

- Data & Digital: Alternative suppliers/buyers mapped, basic scenarios modeled, documents organized for fast retrieval.

Turn this crisis into a concrete checklist your team can actually execute this week.

Use it with your team over the next few days as a working sheet, not a theoretical document.

If you need help interpreting this for your specific sector, lanes, and products, you can reach out by email.

The commitment from me is simple: no hype, no jargon, only the kind of decisions I would make if I were responsible for keeping your business alive.

If you found this useful, share it with at least one MSME owner who needs straight, data‑driven guidance, not noise.

{kind=link}

{kind=link}

{kind=link}